Temenos Announces Continued Strong Q3-21 Momentum With License Growth of 20%, SaaS Revenue Growth of 30% And Bookings Growth of 19%

SaaS revenue growth of 30%

Total Bookings growth of 19%

Total Software Licensing growth of 23%

FCF growth of 19%

Re-confirmed FY-21 guidance

Ad hoc announcement pursuit to Article 53 of the SIX Listing Rules

GENEVA, Switzerland, October 14, 2021 –Temenos AG (SIX: TEMN), the banking software company, today reports its third quarter 2021 results.

The definition of non-IFRS adjustments is below and a full reconciliation of IFRS to non-IFRS results can be found in Appendix II.

*Constant currency (c.c.) adjusts prior year for movements in currencies

Q3 2021 highlights

- Continued strong momentum in the third quarter

- License and SaaS both performed strongly, with SaaS revenue accelerating to 30% and licenses up 20%

- Total Bookings grew 19% in Q3-21 on the back of strong demand across client tiers

- US continued to be the largest contributor to total software licensing in the quarter

- Signings in the US included clients across both SaaS and license

- Sequential improvement in Europe sales, in particular for new SaaS deals

- Acceleration in Europe sales expected in Q4-21 across both license and SaaS

- Two partnerships announced with Banking-as-a-Service providers Mbanq and Vodeno to enter the BaaS market

- Deal signed with Green Dot in the US to build and power the digital bank and fintech’s cloud-based processing platform

- Activity with Tier 1 and 2 banks is increasing, contributing 43% of sales in the quarter

- Strong sales to the installed base in the quarter

- 18 new client wins in the quarter across license and SaaS

- Investing in our people and talent to ensure we are well positioned for future growth

- 12 implementation go-lives in the quarter

- EBIT growth continued to drive operating and free cash flow generation

- Re-confirmed FY 2021 guidance

Q3 2021 financial summary (non-IFRS)

- Total Bookings growth of 19% c.c. in Q3-21

- SaaS Annual Contract Value (ACV) of USD 10.7m in Q3-21

- Annual Recurring Revenue growth of 9% c.c. in Q3-21

- Non-IFRS SaaS & subscription revenue growth of 30% c.c. in Q3-21

- Non-IFRS total software licensing revenues up 23% c.c. in Q3-21

- Non-IFRS total revenue up 9% c.c. in Q3-21

- Non-IFRS EBIT growth of 7% c.c. in Q3-21

- Q3-21 non-IFRS EBIT margin of 37.2%, down 1% points c.c.

- Operating Cash Flow growth of 7% and Free Cash Flow growth of 19% in Q3-21

- Leverage at 2.2x, expected to be at 2.0x by year end

- DSOs at 111 days, flat year-on-year

Commenting on the results, Temenos CEO Max Chuard said:

“The business momentum continued in the third quarter, with the sales environment improving across regions and strong levels of demand across products. The US continued its trajectory from H1-21 and remains the largest contributor to total software licensing, with good levels of demand, both for SaaS and on-premise. Europe also saw a sequential improvement, and was the second largest contributor to SaaS ACV in the quarter. Our ACV in Q3-21 was largely driven by new signings, and overall we see strong demand for SaaS and cloud across our client base and expect this to continue. We also saw strong demand for licenses, which grew 20% year-on-year, and activity levels with Tier 1 and 2 accounts continues to increase.

We announced two partnerships with Banking-as-a-Service providers in the quarter to enter the BaaS market in the US and Europe. Mbanq offers services to Credit Unions in the US, an estimated USD 3.6bn market, and Vodeno is targeting the European BaaS market, estimated at over USD 3bn annually. We also signed a key deal with Green Dot in the US to power its direct digital bank and banking platform services, competing against some of the largest vendors in the US market. We believe that the demand for BaaS will only increase going forward as financial institutions look to accelerate their digital transformation journeys, and fintechs and e-commerce platforms look to embed banking services such as credit, payments, lending and accounts into their ecosystems. This is an exciting and accelerating trend and I am delighted that our technology is at the forefront of this evolving market.

I am confident in the outlook for the balance of the year given the momentum in the business. We had strong growth in Total Bookings in Q3-21 and are ahead of 2019 year-to-date. We have built significant backlog which gives us good visibility into 2022.”

Commenting on the results, Temenos CFO Takis Spiliopoulos said:

“We saw good growth this quarter across both license and SaaS, with several quarters of strong ACV growth reflecting in the P&L. SaaS revenue accelerated to 30% in the quarter as previously indicated and is now starting to better reflect our strong ACV growth from previous quarters. Licenses also grew a very healthy 20% as the business environment continues to normalise. In terms of new bookings, we generated USD 10.7m of SaaS ACV in the quarter and USD153m of Total Bookings, an increase of 19% on last year and adding further to our backlog. ARR grew 9%, driven by both SaaS and 3% growth in maintenance. We expect maintenance to accelerate to mid-to-high single digit growth in the fourth quarter. We also expect further sequential improvement in SaaS revenue of USD 3m in the fourth quarter.

Total revenue grew 9% in the quarter and non-IFRS EBIT grew 7%, delivering a non-IFRS EBIT margin of 37.2%, down 2% point reported.

Our cash generation remains strong, with an operating cash inflow of USD 68m in Q3-21, up 7%, and USD 40m of Free Cash Flow, up 19%. DSOs ended the quarter at 111 days, flat year-on-year, and debt leverage was at 2.2x. We expect our leverage to be at around 2.0x by year end, in line with FY20.

We have reconfirmed our FY-21 guidance, with SaaS ACV expected growth to 50-60%, ARR growth of 10-15%, non-IFRS total software licensing growth of 14% to 18%, and non-IFRS total revenue growth of between 8% and 10%. We are guiding for a 2021 non-IFRS EBIT growth of 12-14%, implying an EBIT margin of 37.1%.”

Revenue

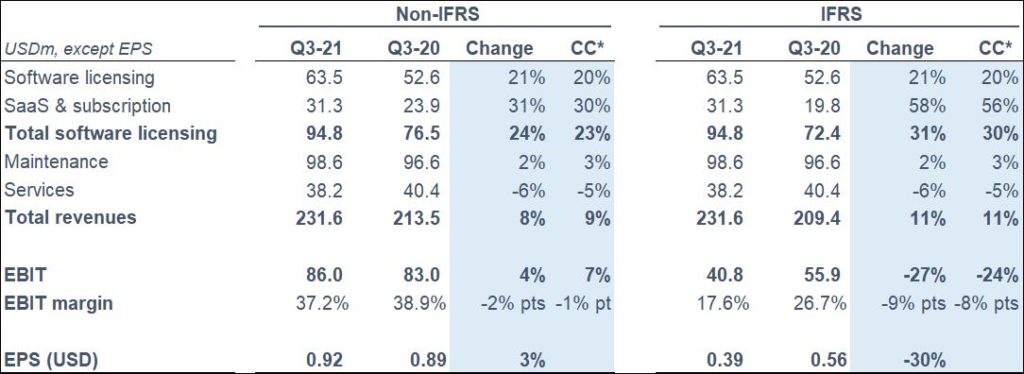

IFRS revenue was USD 231.6m for the quarter, an increase of 11% vs. Q3-20.

Non-IFRS revenue was USD 231.6m for the quarter, an increase of 8% vs. Q3-20.

IFRS total software licensing revenue for the quarter was USD 94.8m, an increase of 31% vs. Q3-20.

Non-IFRS total software licensing revenue was USD 94.8m for the quarter, an increase of 24% vs. Q3-20.

EBIT

IFRS EBIT was USD 40.8m for the quarter, a decrease of 27% vs. Q3-20.

Non-IFRS EBIT was USD 86.0m for the quarter, an increase of 4% vs. Q3-20.

Non-IFRS EBIT margin was 37.2%, down 2% point vs. Q3-20.

Earnings per share (EPS)

IFRS EPS was USD 0.39 for the quarter, a decrease of 30% vs. Q3-20.

Non-IFRS EPS was USD 0.92 for the quarter, an increase of 3% vs. Q3-20.

Cash flow

IFRS operating cash was an inflow of USD 68m in Q3-21 compared to USD 63m in Q3-20, an increase of 7% and representing an LTM conversion of 113% of IFRS EBITDA into operating cash.

USD 40m of Free Cash Flow was generated in the quarter, an increase of 19% vs. Q3-20.

2021 non-IFRS guidance

ARR was included as a new guidance metric for 2021. ARR is Annual Recurring Revenue committed at the end of the period for both SaaS and Maintenance. It includes New Customers, up-sell/cross-sell, and attrition. It only includes the recurring element of the contract and exclude variable elements.

The guidance for 2021 is non-IFRS and in constant currencies.

- SaaS ACV growth of 50-60%

- ARR growth of 10-15%

- Total software licensing growth of 14-18%

- Total revenue growth of 8-10%

- EBIT growth of +12-14% (USD 360-367m), implying 37.1% margin

- 100%+ conversion of EBITDA into operating cash flow

- Expected FY 2021 tax rate of 16% to 18%

- DSOs to be below 105 days by year end

Non-IFRS EBIT is adjusted for share-based payments and related social charges costs going forward. For comparison purposes, the FY-20 EBIT adjustments exclude USD 11m of costs. Estimated FY-21 IFRS2 costs are c.USD 50m of which USD 20-25m is the original plan for the year and USD 26m is related to the introduction of a new one-off LTIP programme extended across an increased number of employees to align a broader segment of the middle and upper management with the overall company performance, and alignment of outstanding years of existing LTIP programmes with new metrics introduced in 2021, as voted on at the May 2021 AGM. The total share-based payment cost in Q3-21 was USD 26.2m.

Currency assumptions for 2021 guidance

In preparing the 2021 guidance, the Company has assumed the following:

- EUR to USD exchange rate of 1.17;

- GBP to USD exchange rate of 1.37; and

- USD to CHF exchange rate of 0.92

Conference call and webcast

At 18.30 CET / 17.30 GMT / 12.30 EST, today, October 14, 2021, Max Chuard, CEO, and Takis Spiliopoulos, CFO, will host a webcast to present the results and offer an update on the business outlook. The webcast can be accessed through the following link:

Please use the webcast in the first instance if at all possible to avoid delays in joining the call. For those who cannot access the webcast, the following dial-in details can be used as an alternative. Please dial-in 15 minutes before the call commences.

Switzerland / Europe: + 41 (0) 58 310 50 00

United Kingdom: + 44 (0) 207 107 06 13

United States: + 1 (1) 631 570 56 13

Non-IFRS financial Information

Readers are cautioned that the supplemental non-IFRS information presented in this press release is subject to inherent limitations. It is not based on any comprehensive set of accounting rules or principles and should not be considered as a substitute for IFRS measurements. Also, the Company’s supplemental non-IFRS financial information may not be comparable to similarly titled non-IFRS measures used by other companies. The Company’s non-IFRS figures exclude share-based payments and related social charges costs, any deferred revenue write-down resulting from acquisitions, discontinued activities that do not qualify as such under IFRS, acquisition related charges such as financing costs, advisory fees and integration costs, charges as a result of the amortisation of acquired intangibles, costs incurred in connection with a restructuring plan implemented and controlled by management, and adjustments made to reflect the associated tax charge relating to the above items.

Note: share-based payments and related social charges costs are considered as non-IFRS adjustments from FY21.

Below are the accounting elements not included in the 2021 non-IFRS guidance.

- FY 2021 estimated share-based payments and related social charges charges of USD 50m

- FY 2021 estimated amortisation of acquired intangibles of USD 50m

- FY 2021 estimated restructuring costs of USD 10-12m

Restructuring costs include realizing R&D, operational and infrastructure efficiencies. These estimates do not include impact of any further acquisitions or restructuring programs commenced after October 14, 2021. The above figures are estimates only and may deviate from expected amounts.

Other definitions

SaaS ACV is Annual Contract Value which is the annual value of incremental business taken in-year. This includes new customers, up-sell and cross-sell. It only includes the recurring element of the contract and excludes variable elements.

Total Bookings includes fair value of license contract value, committed maintenance contract value on license, and SaaS committed contract value. All must be committed and evidenced by duly signed agreements.

Investor and Media Contacts

Adam Synder

Head of Investor Relations, Temenos

+41 22 708 1515 asnyder@temenos.comHaya Herbert-Burns

Teneo for Temenos

+44 203 757 9257 haya.herbertburns@teneo.com